Greetings to you all!

Trumps Tariffs

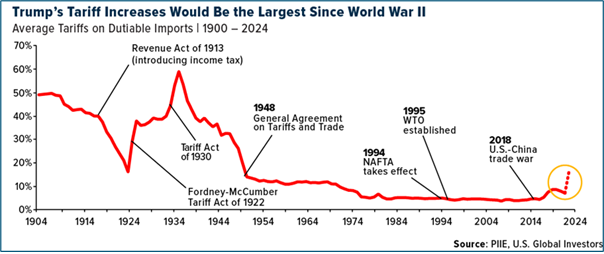

The last few weeks news has been dominated by the start of Donald Trump’s second presidency. With a mandate at all levels of Government for the next two years, rather like a new CEO, he is moving quickly to increase income (through tariffs) and reduce expenses through DOGE (Department of Government Efficiency) and cutting back on funding the war effort in Ukraine.

There is some recent history here as in Trump’s first presidency there was a similar approach to using tariffs to square the ledger with countries “that have been taken advantage of us for years.” I think the intent here is for Trump to get a few quick wins early in his Presidency including getting any bad news out and then looked to stabilise things and reduce tax in the US at a later stage.

Making and reversing decisions on the run his tariff declarations have not been ratified through Congress and threaten to damage relationships with countries the US have historically had very close ties with, especially Canada. While it may seem chaotic, there is an absolute clear strategy here to focus on benefiting US manufacturing at the cost of damaging global trade relationships. In the longer-term tariffs are bad for business and equity markets driving inefficiency and the inevitable retaliation like punching yourself in the head,

Historical US Tariffs

US Equity Market Response

Having reached a new all-time high around mid-February US markets not-unsurprisingly have fallen by approximately 10%, primarily due to the market uncertainty caused by the potential effect of retaliatory tariffs. This decline is not unusual and is certainly within the normal trading patterns of a healthy traded market.

The biggest falls have been in the magnificent seven technology companies many of whose CEO’s have actively been supporting Trump, particularly Elon Musk. At this stage there’s been no cathartic experience of panic selling or a high run of margin calls (no people jumping out of buildings) so in general a period of cautiousness and an understanding that after two very strong years equity markets are more likely to have a more subdued year ahead.

As always investing in equities should be based on the fundamental value of the companies in the portfolio and you should take at least a 5-year view to reduce the effect of short-term government policies impacting the market. If equities do fall further there is an expectation of a Federal Reserve put option where interest rates would fall further than is currently anticipated.

Magnificent 7 Share Price 2025

While there is plenty of financial history and data to refer to in making investment decisions the growth of ETF’s and passive investments has the potential to create much greater volatility in the market then has historically been the case. The VIX (volatility index) remains well contained by historical standards and unless the US goes into a recession markets will trade sideways in the immediate future.

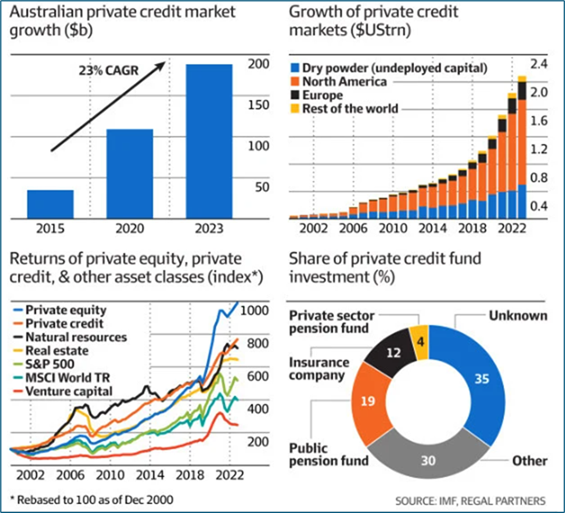

Another new factor is the growth of private equity and private credit as an alternative to listing on the traditional stock markets. This has had the effect of reducing the number of companies on listed markets and a reliance on off market valuations masking the true value of these assets.

Many of the public superfunds in Australia now have 20% to 30% of their assets invested in private equity and private credit which, while smoothing out returns may lead to some of these funds being unable to realise fair value should there be an urgent need for capital?

Growth of Private Equity and Private Credit

Australian Domestic News

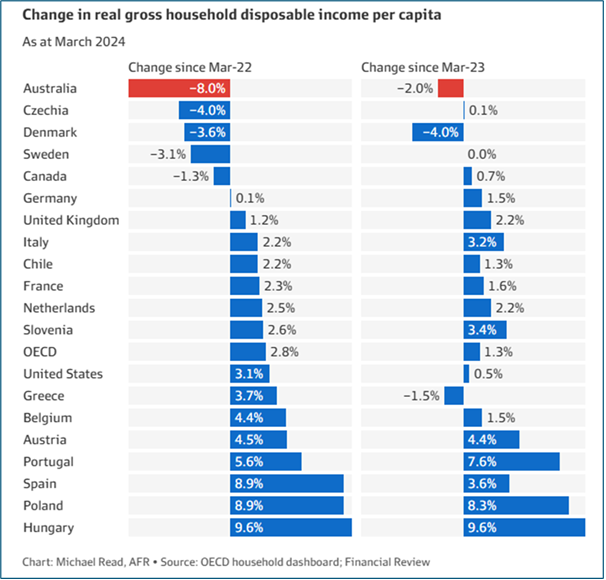

Thankfully, the damages of the Queensland Cyclone were not as bad as had been anticipated and life is returning to normal in the Brisbane area. As a consequence of this there is a delay in the Federal Election to Mid-May to 2O25 and a budget to be introduced on the 25th of March. While the last quarter of CPI was positive at 0.6% we have had seven previous quarters of negative growth per capita which reflects in a loss of purchasing power by Australia of around 8% in 2024.

When looked at a global level this has been a very disappointing for our Country marked by poor productivity and an over reliance on the capital growth of property prices and immigration. We will have a full report on the Budget once released next week and it is anticipated that the election date will be confirmed soon after.

Australian V.S Global Purchasing Power

GST Carve Up

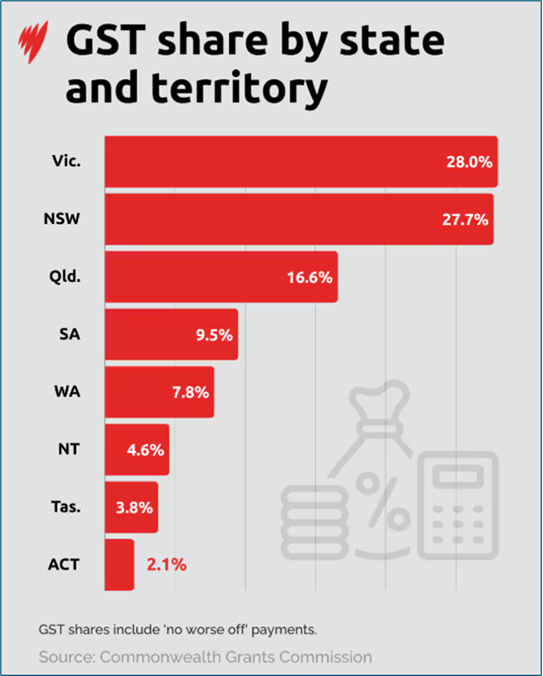

The annual carve up of the GST between the states was announced last week. Possibly counterintuitively Victoria was given a larger part of the pie based on their inability to raise any more taxes while Queensland and to a lesser extent NSW were penalised due to coal royalties while WA again came out as a major net beneficiary.

GST Share By State and Territory

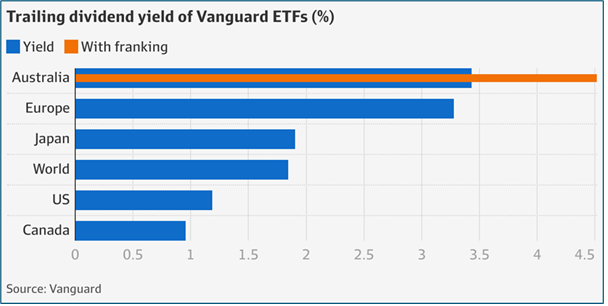

Australian Equity Markets

The dividends declared in the interim season were a little light on compared to previous years mainly due to reductions in the resources sector. The domestic banking sector reflected similar banking results in the US, have declined by approximately 10% from their highs in mid-February importantly their declared Dividends remain solid, and investors will be receiving these over the next few weeks.

I do want to reemphasize that at this stage there have been very few bad debts and that with declining interest rates Australia should avoid any major recession. More positively China has begun to lose much of its own domestic policy which should improve the prospects for our exports to our largest customer.

Australian Dividend Yield

Australian Residential Property

As you might expect with the interest rate drop in February there has been quite an improvement in auction rates in both Sydney and Melbourne reflecting in modestly higher prices. This is particularly so for Melbourne, which has badly underperformed over the last few years and is due a significant catch up on the rest of the country. At this stage, the cost of building new properties is far more expensive than existing ones with approximately 45% going in various levels of Government taxes and Levies.

This continues to lead to an undersupply of new properties to provide accommodation for new migrants into Australia and thus over time you would anticipate existing properties to continue to grow significantly in value. As we move into the Federal Electoral cycle that appears to be very little appetite for significant changes to capital gains tax or negative gearing.

Local News

As you would expect the firm is very busy particularly with pre and post-retirement work for clients in our area. We are prioritising the extended family of existing clients and welcome your inquires as we seek to provide a reliable and consistent financial advice service to our community. Market performance does vary between the years and there is much commentary in social media that is not always that helpful. Often the best investment decisions is to stick to long term asset allocation and risk profiling and allow markets to have a natural stabilising effect over time. If you do have any concerns, we are here to support you and give you accurate, independent advice.

With our best wishes.

Tony and Fiona

Please note this newsletter is of a general nature only. Click to our website

ABN 42 060 673 814 • AFSL No. 407238